Are you struggling to understand how to book a loan in accounting? You’re not alone.

Handling loans in your books can seem tricky, but getting it right is crucial for clear financial records. This guide will break down the process step-by-step, making it simple and straightforward for you. By the end, you’ll know exactly how to record loans properly, avoid common mistakes, and keep your accounts accurate.

Ready to take control of your loan bookkeeping? Let’s dive in.

Credit: discuss.frappe.io

Loan Booking Basics

Booking a loan in accounting means recording the loan details in the financial records. It helps track how much money is borrowed and how much is paid back. Proper booking keeps accounts clear and accurate. This process supports good financial management and helps with reporting.

Understanding the basics of loan booking is important for businesses and individuals. It involves knowing key terms and recognizing different types of loans. These steps make the booking process easier and more precise.

Key Terms In Loan Accounting

Loan accounting uses specific terms to describe the loan process. The principal is the original loan amount borrowed. Interest is the extra money paid to the lender for borrowing. The loan term is the time given to repay the loan. Amortization means paying off the loan over time with regular payments. Finally, collateral is an asset offered to secure the loan.

Types Of Loans In Accounting

Loans come in different forms, each with unique features. A secured loan requires collateral. An unsecured loan does not need collateral but may have higher interest. A fixed-rate loan has the same interest rate throughout the term. A variable-rate loan’s interest can change over time. Knowing these types helps in accurate loan booking and management.

Preparing For Loan Booking

Preparing for loan booking is a crucial step in accounting. It sets the foundation for accurate records and smooth processing. Proper preparation reduces errors and saves time during loan approval.

Careful steps help ensure all details are correct and complete. This preparation protects both the lender and borrower from future issues. Let’s explore the key actions needed before booking a loan.

Gathering Required Documents

Collect all necessary documents before starting the loan booking. These include identity proof, income statements, and credit reports. Having everything ready avoids delays in the process.

Check each document for validity and completeness. Missing or outdated papers can cause problems later. Organize the documents in a clear and logical order for easy access.

Verifying Borrower Information

Confirm all borrower details are accurate and up to date. Verify names, addresses, and contact numbers carefully. Cross-check financial information like income and employment status.

Double-check for any discrepancies or missing data. Accurate information ensures the loan is booked correctly. This step helps prevent future accounting errors and legal issues.

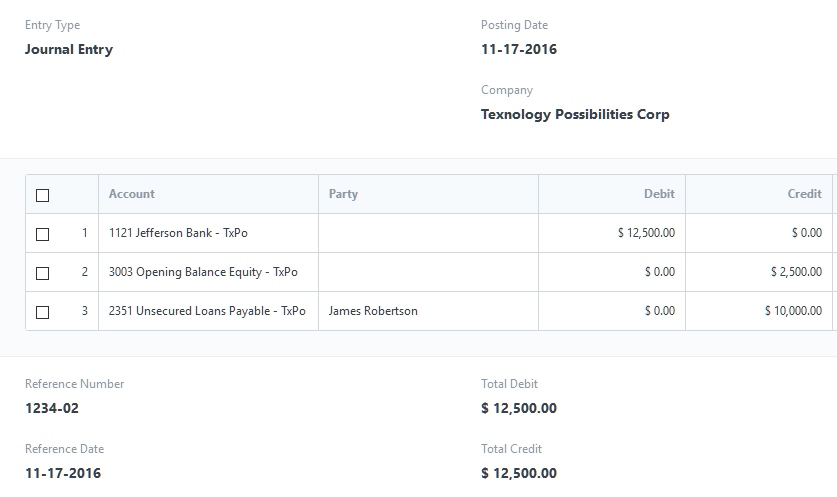

Recording The Loan Entry

Recording a loan entry in accounting is an important step. It shows the loan amount and tracks your debts clearly. Proper recording helps keep your books accurate and organized.

This process involves creating specific accounts and making correct debit and credit entries. Each step ensures the loan appears correctly in your financial records.

Setting Up Loan Accounts

First, create a loan account in your accounting system. This account tracks the loan amount you borrowed. Name it clearly, such as “Loan Payable” or “Loan Receivable.”

Use a liability account if you owe money. Use an asset account if you lent money to someone. This separation helps in easy tracking and reporting.

Debit And Credit Entries

Record the loan by making two entries: one debit and one credit. Debit the cash or bank account to show money received.

Credit the loan account to record your obligation to repay. This keeps the accounting equation balanced. Keep the entries clear and consistent for future reference.

Credit: www.beginner-bookkeeping.com

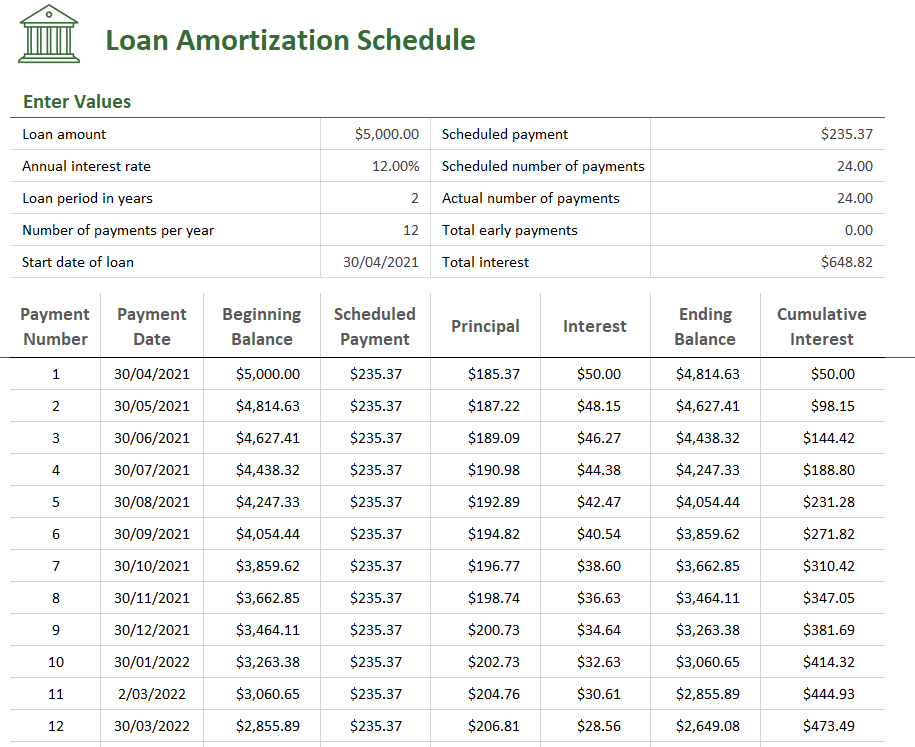

Interest Calculation And Posting

Interest calculation and posting are key parts of managing a loan in accounting. Interest represents the cost of borrowing money. Calculating it correctly ensures accurate financial records. Posting interest means recording it in the accounting system. This process helps track the loan’s cost over time. It also affects profit and loss statements and balance sheets.

Understanding how to calculate and post interest can save time and avoid errors. Different methods exist, and each suits different loan types. Accurate posting keeps accounts updated and transparent for audits.

Methods Of Interest Calculation

Simple interest calculates cost only on the original loan amount. It is easy to compute and common for short-term loans. The formula is principal multiplied by rate and time.

Compound interest adds interest to the principal before calculating more interest. This method increases the total cost over time. It is common for long-term loans and savings accounts.

Another method is the flat rate interest. It applies a fixed percentage on the original loan amount throughout the loan term. This method is straightforward but may not reflect the actual interest cost.

Recording Interest Accruals

Interest accruals record interest that builds up but is not yet paid. This ensures expenses match the time they occur. Accrued interest is recorded as an expense and a liability.

Post journal entries to debit interest expense and credit interest payable. This keeps financial statements accurate. Regular updates help track interest costs and due payments. It also supports better cash flow management.

Loan Repayment Tracking

Tracking loan repayments is a key part of managing loans in accounting. It helps keep your records clear and up to date. Accurate tracking shows how much is paid and what remains. This prevents mistakes and missed payments. Proper tracking also helps with financial planning and budgeting. It gives a clear view of cash flow related to loans.

Recording Installment Payments

Record each loan installment payment as soon as it is made. Note the date and amount paid. Split the payment into principal and interest portions. Update the loan balance after each payment. Use accounting software or a ledger for accuracy. Consistent records help track progress and avoid errors.

Handling Prepayments And Penalties

Prepayments reduce the loan principal faster. Record the extra amount separately from regular payments. Check the loan terms for any penalties on early payments. If penalties apply, record them as expenses. Adjust the loan balance after applying prepayments and penalties. This keeps your accounts correct and transparent.

Credit: quickbooks.intuit.com

Reporting And Compliance

Reporting and compliance are vital in booking a loan in accounting. They ensure transparency and accuracy in financial records. Proper reporting helps track loan details clearly. Compliance guarantees adherence to laws and regulations.

Both reporting and compliance protect businesses from legal risks. They also build trust with stakeholders and financial institutions. Accurate records support better financial decisions and audits.

Generating Loan Reports

Loan reports summarize all loan activities. They include loan amount, interest rate, and repayment schedule. These reports help monitor loan status regularly. They show outstanding balances and payment history. Generating reports often uses accounting software. Reports must be clear and easy to read. Consistent reporting avoids errors and confusion.

Meeting Regulatory Requirements

Regulatory requirements vary by location and loan type. Businesses must follow local accounting standards and loan laws. Compliance involves submitting reports to authorities on time. It also means keeping detailed records for audits. Ignoring regulations can lead to fines or penalties. Staying updated on rules ensures smooth operations. Proper training helps staff understand compliance needs.

Common Mistakes To Avoid

Booking a loan in accounting requires care and attention. Mistakes can lead to errors in financial records. These errors may cause confusion and affect decision-making. Avoiding common mistakes helps keep your books accurate and reliable.

Incorrect Account Classification

Loans must be recorded in the right accounts. Classifying a loan as income or expense is wrong. Loans are liabilities and should be listed as such. Misclassifying loans distorts your financial position. Always check if you use the correct loan account.

Ignoring Interest Adjustments

Interest on loans changes over time. Not updating interest expenses can cause errors. Interest adjustments affect your profit and loss statements. Record interest expenses regularly and accurately. This practice keeps your accounts truthful and up to date.

Using Accounting Software

Using accounting software simplifies the process of booking a loan. It helps track loan details clearly and keeps records organized. Software reduces errors and saves time for accountants and business owners.

Many software options offer features to record loan amounts, interest rates, and payment schedules. These tools can generate reports and reminders for loan payments. This makes managing loans easier and more accurate.

Popular Tools For Loan Management

QuickBooks is widely used for its easy loan tracking features. Xero offers clear dashboards to monitor loan balances and payments. FreshBooks helps small businesses with simple loan entries and reports. Zoho Books provides loan templates and automated calculations. These tools suit different business sizes and needs.

Automation Benefits

Automation cuts down manual data entry and human mistakes. It updates loan balances automatically after each payment. Alerts remind users about due dates to avoid late fees. Reports generate instantly to show loan status and history. Automation improves accuracy and saves valuable time.

Frequently Asked Questions

What Is The Process To Book A Loan In Accounting?

Booking a loan involves recording the loan amount as a liability. Debit the cash or bank account and credit the loan payable account. This ensures accurate tracking of borrowed funds and repayment obligations in financial records.

How To Record Loan Interest In Accounting Entries?

Loan interest is recorded as an expense. Debit the interest expense account and credit the loan payable or cash account when interest is paid. This keeps financial statements accurate and reflects borrowing costs correctly.

Which Accounts Are Affected When Booking A Loan?

The main accounts are the cash or bank account and the loan payable account. When booking a loan, debit cash and credit loan payable. Interest payments affect interest expense and cash or loan payable accounts.

Why Is Accurate Loan Booking Important In Accounting?

Accurate loan booking ensures financial statements reflect true liabilities. It helps in budgeting, auditing, and compliance with accounting standards. Proper recording prevents errors in financial analysis and decision-making.

Conclusion

Booking a loan in accounting is simple with the right steps. Always record the loan clearly in your books. Keep track of payments and interest carefully. This helps avoid mistakes and confusion later. Accurate records show your true financial position.

Stay consistent and review entries often. This practice supports better financial decisions. Following these tips makes loan booking easy and clear. Your accounting will stay organized and reliable.